By MARTIN KALAYDJIAN

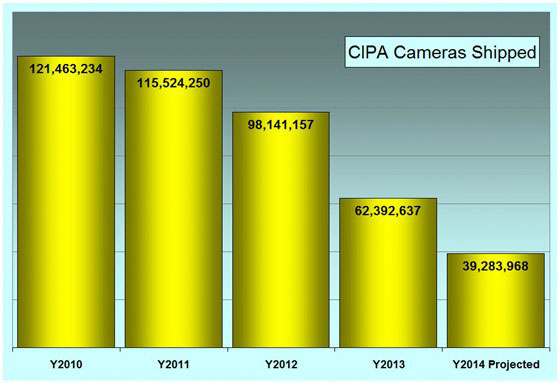

I just took a look at the CIPA shipment numbers for April 2014, and they really are depressing. CIPA reports that new camera shipments continue to fall, losing about a third of their market each year. This isn’t meant to be about doom and gloom. It is only “crying wolf” if the wolf never shows up. In this case, the wolf is here, and has been here for the past four years. The wolf doesn’t seem to be going away. So this is just a discussion of the new reality facing photo enthusiasts, and the likely results that will come from this change.

The actual number shipped from January to April was a little over 13 million. Since it was a four month period, I projected it for the year. The actual shipment number could be higher or lower. Higher if end of year holiday sales are much higher than 2013, or lower if the same pattern of decline continues for the next eight months. But one thing for sure, it won’t be the same.

If this trend continues much longer, we will have a a very different future to look forward to. There will always be millions of people who prefer using real cameras to take photos, rather than cell phones or tablets. They aren’t going away. But there will be a lot fewer of us in the future. So the industry will have to adjust to that.

The problem isn’t just those cheap point-and-shoot cameras that we have little use for, and won’t miss. This trend is happening with all cameras. The down trend is also happening with interchangeable lens cameras, although not to the same degree.

The ILC shipments peaked in 2012, and have been declining ever since. ILC volume is about where it was four years ago. A product that entered the mass market ten years ago is now leaving it, and will become just another niche product for enthusiasts.

And remember, this is all happening while the world population continues to grow, and there are more middle class people in third world nations with more disposable income for things like cameras.

These changes will have a profound affect on the industry, and to users in general. There is nothing anyone can do to reverse this trend, but the manufacturers still need to make strategic decisions to deal with it. At least if the camera makers want to stay in business.

What happens next is fairly predictable, and many of these things have already happened:

- There will be draconian cost cutting by all camera makers. Even the market leaders are way down, so they will also have to cut labor and material costs, manage marketing budgets better. If Canon had a 40% market share four years ago, then it was 40% of 120 million units. If they still have a 40% market share, then it is 40% of around 40 million units. This is a major sea change for the market leaders as well as the smaller competitors.

- There will probably be some market consolidation. There may be more mergers, acquisitions and alliances, as the makers have to compete for fewer customers. Digital Imaging is now a mature technology, and is in about the same place where automobiles were in the 1920s. Back then there were over 100 different car manufacturers. Today there are less than 20. All of those GM model lines were once separate companies that were acquired by GM (Chevrolet, Oldsmobile, Buick, Pontiac, etc.) 600 local breweries became a small group of major brewers. A few hundred soft drink companies became “Coke, Pepsi and generic store brands.”

- Manufacturers will flee to the high end of the market, where profit margins are greatest. While they have pretty much ceeded the low end P&S market to mobile devices, the entry level ILC could be next, as cell phone makers create changeable lens devices for their products. Of all categories, the ILC has decreased the least, although it is still in decline. ILCs now represent 31% of units shipped, as opposed to 10.6% in 2010. Leica seems to be the maker best positioned going forward, and Casio the one in the worst spot, since they have no ILC products at all. ILC aren’t more profitable because the cameras cost more, they are more profitable because once you buy one you become a lens customer. And now you are committed to one brand only, since each lens mount is largely proprietary. Lenses are a whole lot more profitable than camera bodies are, especially at the high end.

- The industry will have to find and develop more niches in order to survive. And they are doing this as we speak. Any device that has features that are hard to duplicate with a cell phone ap will gain at the expense of those which are easy to duplicate. The number of superzoom (or more appropriately… ultrazoom) cameras sold has sky rocketed. So have waterproof rugged cameras. Cell phones are now using software to duplicate shallow DOF and their users don’t seem to mind the the poor quality of the results. Those users may never come back, because for them convenience always trumps quality.

- Almost no one makes prints anymore. Those ubiquitous giant printing machines that used to churn out 4×6 inch prints have all but disappeared from drug stores and supermarkets. If you want a few small prints today, you don’t have to wait to get them in an hour. You just insert a memory card or thumb drive into a machine at Walmart, and a printer will spit them out in four minutes. And for around 20 cents per print. The days of the booklet of 24 or 36 small prints is long over. Photo sharing today means “the internet” or passing around a cell phone or tablet. Prints themselves have become a high end market for those requiring really large prints. Once the mass market stops needing prints, then they they no longer need anything better than a cell phone for their Facebook pages or web blogs.

- The MILC camera is here to stay. Yes, the overall shippment number has declined a little from a few years ago when the product was brand new, and now that the pipeline had to be filled. As a mature product, new sales are being generated by upgrades, rather than by new users. Still… one in five ILC cameras shipped today is a MILC camera, and this product didn’t even exist six years ago. There really is a trend to smaller and lighter, witnessed by the arrival of the mini DSLR (Canon SL1). This market segment is so significant that virtually every manufacturer has tried to launch a MILC line (with varying degrees of success), and more MILC cameras are released than SLRs today. The Dpreview camera timeline tells us that so far in 2014 there were 18 ILC cameras announced. A whopping 13 of them (72%) were MILC cameras. This tells you something, even if they are being outsold by SLRs four to one. The manufacturers are clearly betting on this new product, probably because they haven’t come up with anything better to attract younger buyers.

The sky really isn’t falling… it is just changing a lot. And these changes will impact the industry a lot in the next ten years. It will be interesting to see where we end up ten years from now.

What do you think?

This article first appeared on Martin’s photography blog Decent Exposures.